As is customary at this time, the WCPFC Regular Session of the Scientific Committee meets in Manila this year. A wealth of papers covering all aspects of the stocks and bycatch status of the species the WCPFC deals with are readily available for exploration.

I always look forward to the Overview of tuna fisheries in the Western and Central Pacific Ocean, including economic conditions. The 2023 version was compiled by three people I know and for whom I have the ultimate respect: Tiffany Vidal, Peter Williams from SPC, and Thomas Ruaia from FFA.

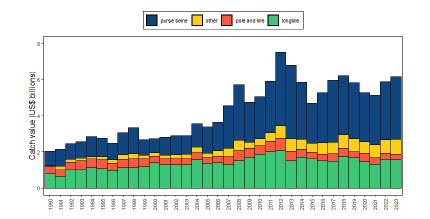

Catch value of albacore, bigeye, skipjack and yellowfin in the WCPFC–CA, by longline, pole-and-line, purse seine and other gear types

The publication shows our current situation regarding fisheries, fishing efforts, and the economic conditions in which they work.

This report should be compulsory reading for everyone who wants to say anything about the fisheries in the WCPO (I’m looking at you NGOs)

Dive into the full text and the great graphs, I just quote the abstract below.

This paper broadly describes the major fisheries in the WCPFC Statistical Area (WCPFC-CA), highlighting activities during the most recent calendar year (2023) and covering the most recent summary of catch estimates by gear and species.

The provisional total WCPFC–CA tuna catch for 2023 was estimated at 2,630,858 mt, slightly lower than the 2022 level (2,702,099 mt) and around 342,728 mt lower than the record catch in 2019 (2,973,586 mt). The WCPFC–CA tuna catch (2,630,858 mt) for 2023 represented 79% of the total Pacific Ocean tuna catch of 3,310,318 mt, and 52% of the global tuna catch (the provisional estimate for 2023 is 5,027,799 mt), noting that unlike other oceans, over 80% of the WCPFC–CA tuna catch occurs in the waters of coastal states.

The 2023 WCPFC–CA catch of skipjack (1,647,702 mt – 63% of the total catch) was around 397,077 mt lower than the record in 2019 (2,044,779 mt). The WCPFC–CA yellowfin catch for 2023 (746,913 mt – 28%) was a decrease of 7,457 mt from the record 2021 catch (754,370 mt), noting that 2023 yellowfin catches are the second highest on record. The recent high catches are partially due to the high catch levels from the ‘other’ category (primarily small-scale fisheries in Indonesia).

The WCPFC–CA bigeye catch for 2023 (140,309 mt – 5%) was again one of the lowest of the time series, but relatively consistent with the catch levels from the previous two years. The 2023 WCPFC–CA albacore catch (94,934 mt – 4%) was around 2,741 mt higher than in 2022, but catches from 2021-2023 are the lowest on record since 1997. The provisional South Pacific albacore catch in 2023 was 67,751 mt; however, this estimate is expected to increase with the addition of catches from the Eastern Pacific Ocean, which have not yet been received.

The provisional 2023 purse seine catch of 1,843,100 mt was around 257,000 mt lower than the record catch in 2019 (2,100,135 mt). With respect to species specific purse seine catches, skipjack (1,377,830 mt: 75% of the catch) was slightly below the recent 10-year average, yellowfin tuna (408,281 mt; 22% of the total purse seine tuna catch) was around 92,000 mt lower than the record catch in 2017 (500,506 mt) and the fourth highest annual catch on record, the provisional catch estimate for bigeye tuna for 2023 (56,094 mt) was about 8,500 mt lower than the 2022 catch and a only a slight increase over the notably low purse seine bigeye tuna catch in 2019 (52,081 mt). The increased bigeye tuna catches since 2020 appears to be related to a higher number of associated sets.

The provisional 2023 pole-and-line catch (143,431 mt) is the lowest annual catch since the early- 1960s, due to reduced catches in the Japanese fishery, although we note as in previous years the provisional nature of the estimates at this stage

The provisional WCPFC–CA longline catch (234,894 mt) for 2023 remains lower than the average over the previous decade but a slight increase from 2022 (243,115 mt). The bigeye component of the longline fishery (56,203 mt) was similar to the 2022 catch level - which are some of the lowest catches reported since the mid-1980s. Both albacore and yellowfin catches were higher in 2023 than in 2022.

The 2023 South Pacific troll albacore catch (1,192 mt) was the second lowest catch level since 1980 (744 mt were reported in 1983), largely owing to a contraction in NZ’s troll fleet operating in the region. The New Zealand troll fleet (94 vessels catching 864 mt in 2023) and the United States troll fleet (10 vessels catching 328 mt in 2023) accounted for all of the 2023 albacore troll catch, although minor contributions also come from the Canadian, the Cook Islands and French Polynesian fleets when their fleets are active in this fishery

In 2023, market prices for purse seine-caught products increased. Thai imports averaged $1,773/mt, marking an 8% increase from 2022, while Yaizu prices increased by 12% to $1,923/mt.

Conversely, prices for longline-caught yellowfin decreased across all markets. In Yaizu, prices fell by 28% to $5.07/kg. Prices for fresh and frozen yellowfin from selected ports decreased by 17% to $7.33/kg and 26% to $5.60/kg, respectively. The price from Oceania also declined by 5% to $8.51/kg, partly due to the appreciation of the US dollar against the Japanese yen.

Prices for longline-caught bigeye also declined across most markets except Oceania. In Japan, average prices from selected ports for fresh bigeye fell by 7% to $12.29/kg, and frozen bigeye decreased by 25% to $7.11/kg. However, the price for fresh imports from Oceania increased by 8% to $14.11/kg. In the U.S, fresh bigeye import prices rose by 4% to a record high of $12.03/kg in 2022, before slightly declining by 4% to $11.19/kg in 2023. Thai import prices for albacore decreased by 10% to $3.19/kg in 2023. Similarly, US fresh prices declined by 5% to $5.63/kg, and Japanese selected ports fresh prices fell by 20% to $3.24/kg.

In 2023, the total estimated delivered value of the tuna catch in the WCPFC-CA increased marginally by 4% to $6.1 billion. The purse seine fishery, valued at $3.5 billion, saw a 7% rise from 2022, representing 56% of the total value. In contrast, the longline fishery’s value decreased slightly by 1% to $1.6 billion, while the pole and line catch value dropped by 11% to $312 million, attributed to reduced catches and a decline in the Yaizu price for pole-and-line-caught skipjack. Conversely, the value of catches from other gears increased by 11%, reaching $820 million.

In 2023, the WCPFC-CA skipjack catch was valued at $3 billion, a marginal 2% increase from the previous year, and accounted for nearly half of the total tuna catch value. The value of the albacore tuna catch decreased by 9% to $304 million, while the values for yellowfin and bigeye catches increased to $2.1 billion (+10%) and $784 million (+4%), respectively.

In 2023, economic conditions across purse seine, tropical longline, and southern longline fisheries in the WCPFC-CA improved compared with 2022. The tropical purse seine index improved, remaining above average at 109, driven by rising fish prices and declining fuel costs. From 2018 to 2020, this index stayed considerably above its 20-year average, primarily due to high catch rates. In 2022, the index dropped to 98, its lowest level since 2014. However, it rebounded in 2023, driven by an increase in fish prices, declining fuel costs and higher catch rates.

For the southern longline fishery, 2023 saw a positive trend with the index approaching its 20-year average, supported by higher catch rates and lower fuel prices. Similarly, the economic conditions for the tropical longline fishery improved, nearing the 20-year average, driven by increased catch rates and a decrease in fuel prices.