It comes out a few weeks later than usual, yet SPC’s flagship tuna publication, “The Western and Central Pacific Tuna Fishery: 2023 Overview and Status of Stocks,” is out.

The publication always has well-crafted graphs and tables (Plus now pictures, many of them mine), with some information immediately apparent and others requiring closer reading.

The news still talks about the collapse of tuna fisheries in the Pacific, that the (name your geopolitical nemesis, i.e., China, the US, Korea, Japan, EU, etc.) are taking all the fish, that the regional management organisations are secret, that we need eco-labels to know if fisheries are sustainable, and so on. So… Do you want to rely on the multimillion-dollar spin industry for information, or do you prefer to read a document that links all the scientific evidence supporting their claims?

This document includes an analysis of the fishery by species and fleet type, the impact of climate change and much more.

Like most things in life, there is good and bad news. Some things are going well, while others are not. However, if you look closely, you can see beyond the surface.

If you're reading this blog, it's probably because you're interested in tuna fisheries in the region. SPC is the data and science provider for the WCPFC and has some of the top stock assessment scientists in the world. Therefore, this publication is essential reading for any informed discussion.

What are the things I rescue?

Catch Data Overview:

The 2023 catch was 2,623,966 metric tonnes, a 1.3% decrease from 2022, representing 53% of the global tuna catch.

Species-Specific Catch Trends:

Skipjack tuna has consistently been the most caught species, with significant contributions from purse-seine and pole-and-line methods, accounting for 62% of the total catch in 2023.

Yellowfin tuna catches have shown variability, with a 7% increase from 2022, making up 28% of the total catch.

Bigeye tuna catches have shown variability, with a 1% decrease from 2022, making up 6% of the total catch.

South Pacific albacore catches are predominantly from longline gear, with a 3% increase from 2022, making up 4% of the total catch.

Gear Type Contributions:

Purse-seine: 1,837,030 t (70% of total catch)

Longline: 227,646 t (9% of total catch)

Pole-and-line: 111,670 t (4% of total catch)

Troll: 6,925 t (<1% of total catch)

Other gear: 440,695 t (17% of total catch)

Fishing Effort and Fleet Data:

The report includes indices of fishing effort, such as the number of vessels, days, and sets for purse-seine, longline, and pole-and-line fisheries.

Effort data exclude certain domestic fleets (e.g., Japan coastal, Indonesia, Philippines, and Vietnam).

Biological Reference Points and Stock Status:

The report provides the latest stock assessments for South Pacific albacore, bigeye, skipjack, and yellowfin tunas, including spawning biomass, maximum sustainable yield (MSY), and fishing mortality ratios.

Skipjack, yellowfin, and South Pacific albacore stocks are not overfished and are not experiencing overfishing.

Bigeye tuna has a 12.5% probability of undergoing overfishing.

Harvest Strategy Development:

Progress varies across the four key tuna stocks.

A management procedure for skipjack tuna was adopted in 2022.

Interim target reference points (TRPs) and candidate TRPs have been identified for South Pacific albacore and bigeye tuna, respectively.

Tagging Projects:

Data on the number of tuna tagged and recovered during major tagging projects (SSAP, RTTP, PTTP) are included, highlighting efforts to monitor tuna movements and population dynamics.

Ecosystem Considerations:

Observer coverage for purse-seine and longline fleets has increased, with purse-seine coverage reaching nearly 60% in 2023.

Bycatch rates and interactions with species of special interest, such as marine mammals and seabirds, are being monitored and managed.

Climate and Ecosystem Indicators:

The report discusses climate indices and their impact on the oceanic environment, including sea surface temperature anomalies and the El Niño Southern Oscillation (ENSO).

Climate change projections for tuna biomass under different greenhouse gas emission scenarios (RCP2.6 and RCP8.5) are presented, indicating potential shifts in tuna distribution and abundance by 2050.

And, of course, my favourite graph

Majuro (top left) and Kobe (top right) plot stock status summary for the four WCPO target tuna stocks and a comparison of Kobe plot stock status for the same four tuna species in the other major ocean basins

These are my least favourites, as both relate to the mess that Longline continues to be in the region (even if it is one of the gears that I liked—and challenged me—the most while fishing commercially until 1998).

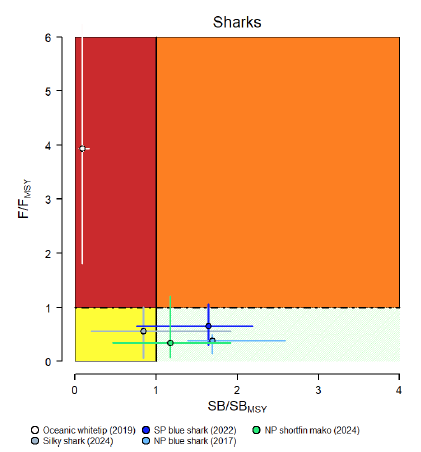

The status of billfishes and sharks

In the one below (page 52), you see fishing effort, in fleet sizes and number of hooks fished (bottom), for the longline fishery in the WCPFC.

When I was fishing these waters in 1993/4, it was the heyday of LL in the WCPO, peaking at 5000 vessels. Today, as you can see, there are only around 2000 left, yet they are soaking 200 million more hooks. How can that be possible? Deck and gear setting technology are almost the same.

Response: overworking crew. The workload has been duplicated (and their payment is below 25% of what I was paid at the time in nominal terms)

Now if you really want to get depressed… read the climate change section :-(