Every two years my former employer FAO (Food and Agriculture Organisation of the Unites Nations) publishes its report over the state of fisheries and aquaculture worldwide. Is the best source of information available on the topic, here are some of it key findings.

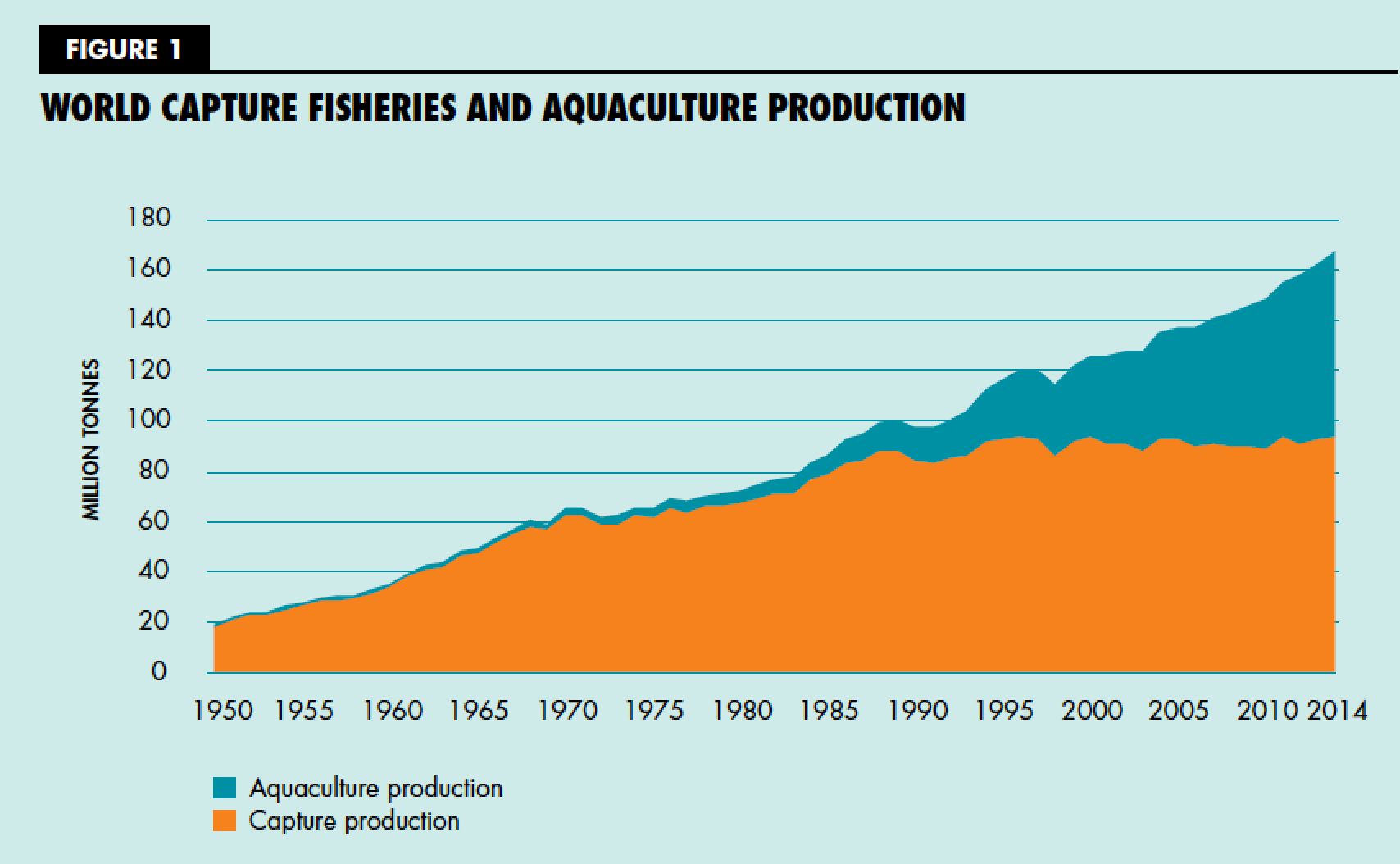

We are faced with one of the world’s greatest challenges – how to feed more than 9 billion people by 2050 in a context of climate change, economic and financial uncertainty, and growing competition for natural resources. Hence meeting the ever-growing demand for fish as food will be imperative, and also immensely challenging. With capture fishery production relatively static since the late 1980s, aquaculture has been responsible for the impressive growth in the supply of fish for human consumption.

Growth in the global supply of fish for human consumption has outpaced population growth in the past five decades, increasing at an average annual rate of 3.2 percent in the period 1961– 2013, double that of population growth, resulting in increasing average per capita availability.

The state of the world’s marine fish stocks has not improved overall, despite notable progress in some areas. Based on FAO’s analysis of assessed commercial fish stocks, the share of fish stocks within biologically sustainable levels decreased from 90 percent in 1974 to 68.6 percent in 2013. Thus, 31.4 percent of fish stocks were estimated as fished at a biologically unsustainable level and therefore overfished. Of the total number of stocks assessed in 2013, fully fished stocks accounted for 58.1 percent and underfished stocks 10.5 percent. The underfished stocks decreased almost continuously from 1974 to 2013, but the fully fished stocks decreased from 1974 to 1989, and then increased to 58.1 percent in 2013. Correspondingly, the percentage of stocks fished at biologically unsustainable levels increased, especially in the late 1970s and 1980s, from 10 percent in 1974 to 26 percent in 1989. After 1990, the number of stocks fished at unsustainable levels continued to increase, albeit more slowly. The ten most-productive species accounted for about 27 percent of the world’s marine capture fisheries production in 2013. However, most of their stocks are fully fished with no potential for increases in production; the remainder are overfished with increases in their production only possible after successful stock restoration.

Global total capture fishery production in 2014 was 93.4 million tonnes, of which 81.5 million tonnes from marine waters and 11.9 million tonnes from inland waters For marine fisheries production, China remained the major producer followed by Indonesia, the United States of America and the Russian Federation. Catches of anchoveta in Peru fell to 2.3 million tonnes in 2014 – half that of the previous year and the lowest level since the strong El Niño in 1998 – but in 2015 they had already recovered to more than 3.6 million tonnes. For the first time since 1998, anchoveta was not the top-ranked species in terms of catch as it fell below Alaska pollock.

The Northwest Pacific remained the most productive area for capture fisheries, followed by the Western Central Pacific, the Northeast Atlantic and the Eastern Indian Ocean. With the exception of the Northeast Atlantic, these areas have shown increases in catches compared with the average for the decade 2003–2012.

Four highly valuable groups (tunas, lobsters, shrimps and cephalopods) registered new record catches in 2014. Total catches of tuna and tuna like species were almost 7.7 million tonnes.

World per capita apparent fish consumption increased from an average of 9.9 kg in the 1960s to 14.4 kg in the 1990s and 19.7 kg in 2013, with preliminary estimates for 2014 and 2015 pointing towards further growth beyond 20 kg.

An estimated 56.6 million people were engaged in the primary sector of capture fisheries and aquaculture in 2014, of whom 36 percent were engaged full time, 23 percent part time, and the remainder were either occasional fishers or of unspecified status. Following a long upward trend, numbers have remained relatively stable since 2010, while the proportion of these workers engaged in aquaculture increased from 17 percent in 1990 to 33 percent in 2014. In 2014, 84 percent of the global population engaged in the fisheries and aquaculture sector was in Asia, followed by Africa (10 percent), and Latin America and the Caribbean (4 percent). Of the 18 million people engaged in fish farming, 94 percent were in Asia.

Women accounted for 19 percent of all people directly engaged in the primary sector in 2014, but when the secondary sector (e.g. processing, trading) is included women make up about half of the workforce.

The total number of fishing vessels in the world in 2014 is estimated at about 4.6 million, very close to the figure for 2012. The f leet in Asia was the largest, consisting of 3.5 million vessels and accounting for 75 percent of the global f leet, followed by Africa (15 percent), Latin America and the Caribbean (6 percent), North America (2 percent) and Europe (2 percent). Globally, 64 percent of reported fishing vessels were engine-powered in 2014, of which 80 percent were in Asia, with the remaining regions all under 10 percent each. In 2014, about 85 percent of the world’s motorized fishing vessels were less than 12 m in length overall (LOA), and these small vessels dominated in all regions. The estimated number of fishing vessels of 24 m and longer operating in marine waters in 2014 was about 64 000, the same as in 2012.

The share of world fish production utilized for direct human consumption has increased significantly in recent decades, up from 67 percent in the 1960s to 87 percent, or more than 146 million tonnes, in 2014. The remaining 21 million tonnes was destined for non-food products, of which 76 percent was reduced to fishmeal and fish oil in 2014, the rest being largely utilized for a variety of purposes including as raw material for direct feeding in aquaculture. Increasingly, the utilization of by-products is becoming an important industry, with a growing focus on their handling in a controlled, safe and hygienic way, thereby also reducing waste.

In 2014, 46 percent (67 million tonnes) of the fish for direct human consumption was in the form of live, fresh or chilled fish, which in some markets are the most preferred and highly priced forms.

The rest of the production for edible purposes was in different processed forms, with about 12 percent (17 million tonnes) in dried, salted, smoked or other cured forms, 13 percent (19 million tonnes) in prepared and preserved forms, and 30 percent (about 44 million tonnes) in frozen form. Freezing is the main method of processing fish for human consumption, and it accounted for 55 percent of total processed fish for human consumption and 26 percent of total fish production in 2014.

Fishmeal and fish oil are still considered the most nutritious and digestible ingredients for farmed fish feeds. To offset their high prices, as feed demand increases, the amount of fishmeal and fish oil used in compound feeds for aquaculture has shown a clear downward trend, with their being more selectively used as strategic ingredients at lower concentrations and for specific stages of production, particularly hatchery, broodstock and finishing diets.

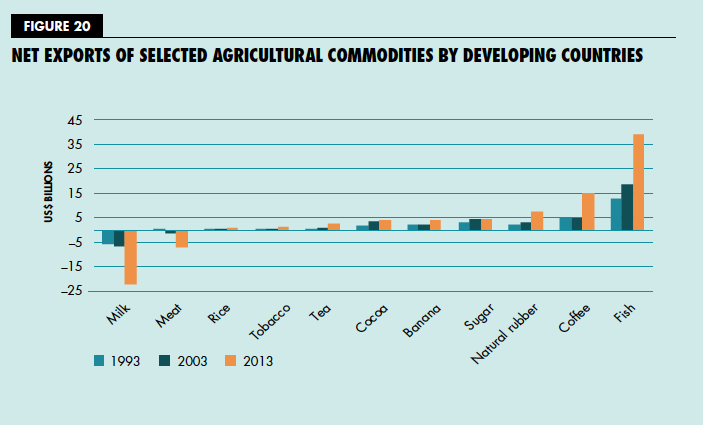

International trade plays a major role in the fisheries and aquaculture sector as an employment creator, food supplier, income generator, and contributor to economic growth and development, as well as to food and nutrition security. Fish and fishery products represent one of the most-traded segments of the world food sector, with about 78 percent of seafood products estimated to be exposed to international trade competition. For many countries and for numerous coastal and iverine regions, exports of fish and fishery products are essential to their economies, accounting for more than 40 percent of the total value of traded commodities in some island countries, and globally representing more than 9 percent of total agricultural exports and 1 percent of world merchandise trade in value terms. Trade in fish and fishery products has expanded considerably in recent decades, fuelled by growing fishery production and driven by high demand, with the fisheries sector operating in an increasingly globalized environment. In addition, there is an important trade in fisheries services.

Developing economies, whose exports represented just 37 percent of world trade in 1976, saw their share rise to 54 percent of total fishery export value and 60 percent of the quantity (live weight) by 2014. Fishery trade represents a significant source of foreign currency earnings for many developing countries, in addition to its important role in income generation, employment, food security and nutrition. In 2014, fishery exports from developing countries were valued at US$80 billion, and their fishery net export revenues (exports minus imports) reached US$42 billion, higher than other major agricultural commodities (such as meat, tobacco, rice and sugar) combined.

Here are the words of Manuel Barange, FAO Director of Fisheries and Aquaculture Policy and Resources Division,